Demos

Demos  Colors

Colors

Docs

Docs  Support

Support

Home 15

Newly Added

In the world of real estate investing, your profit isn’t just determined by the rent you collect or the appreciation of your property. The real “secret sauce” to long term wealth in this industry is how effectively you manage your tax strategy. At LIT Nexus, we often see property owners working incredibly hard to increase their monthly income by a few hundred dollars, while simultaneously losing thousands of dollars every year simply because they aren’t claiming the deductions they are legally entitled to.

As we move through the 2026 tax year, the regulations surrounding property management and investment income have become more nuanced. Whether you own a single rental condo in Toronto, a multi-family unit in Illinois, or commercial space in Mohali, understanding the art of the “write-off” is essential.

Here is a deep dive into the most common (and some of the most overlooked) tax deductions for real estate investors.

If you aren’t claiming depreciation, you are missing out on perhaps the single greatest tax benefit of real estate. Unlike most expenses that require you to spend cash today, depreciation is a non cash deduction. It is based on the idea that the building itselfnot the landis wearing out over time and losing value.

In many jurisdictions, you can deduct a portion of the cost of the building every year for decades. This effectively lowers your taxable income without you actually having to take a dollar out of your bank account. However, calculating the exact basis (separating the value of the land from the structure) requires precision. One small error here can lead to an audit or a missed opportunity for significant savings.

For most investors, the largest recurring expense is the mortgage. While you cannot deduct the portion of your payment that goes toward the principal (the equity you are building), you can generally deduct 100% of the interest paid on loans used to acquire or improve the property.

This does not just apply to your primary mortgage. If you have taken out a home equity line of credit (HELOC) to renovate a kitchen or used a credit card to purchase appliances for a rental unit, the interest on those specific business expenses is usually deductible as well. At LIT Nexus, we help our clients track these interest payments meticulously so that every cent of borrowing cost is accounted for come tax season.

This is where many real estate investors run into trouble with tax authorities. There is a legal difference between a “repair” and an “improvement,” and they are treated very differently on your tax return.

Distinguishing between the two is vital. Claiming an improvement as a repair might get you a bigger deduction today, but it could lead to penalties if the tax office decides it should have been capitalized.

Running a rental property is a business, and every business needs a support team. The fees you pay to professionals are fully deductible. This includes:

Many investors forget that even the software they use to track their propertieslike QuickBooks or specialized property management platformsis a deductible business expense.

Do you drive to your rental property to collect rent, perform maintenance, or show the unit to prospective tenants? If so, your local travel is deductible. You can either track your actual expenses (gas, oil, repairs) or use the standard mileage rate set by your local tax authority.

Furthermore, if you have a dedicated space in your home where you conduct your real estate business managing records, taking calls from contractors, or paying billsyou may be eligible for a home office deduction. This allows you to write off a portion of your own home’s utilities, insurance, and even internet costs.

Just like interest, the insurance premiums you pay to protect your investment are a legitimate business expense. This includes landlord liability insurance and fire/theft coverage.

Additionally, if you pay for any utilities that are not reimbursed by your tenantssuch as water, trash collection, or electricity for common areasthese are deductible. Even if the tenant eventually pays you back for them, the initial cost is an expense that must be tracked through your bookkeeping.

You could be eligible for every deduction on this list, but if you do not have the documentation to prove it, those deductions are worthless in the eyes of the tax man. The key to maximizing your write-offs is proactive, year-round bookkeeping.

Waiting until April to dig through a shoebox of faded receipts is not a strategy; it is a recipe for stress and missed savings. At LIT Nexus, we provide the smart solutions and experienced consultancy needed to ensure that every single deductible dollar is captured in real time.

We serve clients across the USA, Canada, and India, navigating the complex global regulations that real estate investors face. Our team ensures your financial records are secure, accurate, and always ready for tax season.

Don’t let your hard earned profits slip away due to poor financial planning. Whether you are a seasoned contractor with a growing portfolio or a first time landlord, LIT Nexus is here to provide the peace of mind you deserve.Ready to optimize your property accounting? Contact us today to see how our dedicated team can streamline your bookkeeping and maximize your tax returns for the 2026-27 session.

Introduction The accounting industry is evolving rapidly, and CPA firms are facing increasing pressure to…

Introduction The accounting industry is becoming increasingly competitive as businesses demand faster service, greater financial…

Introduction The accounting industry is evolving rapidly as CPA firms face increasing client expectations, tighter…

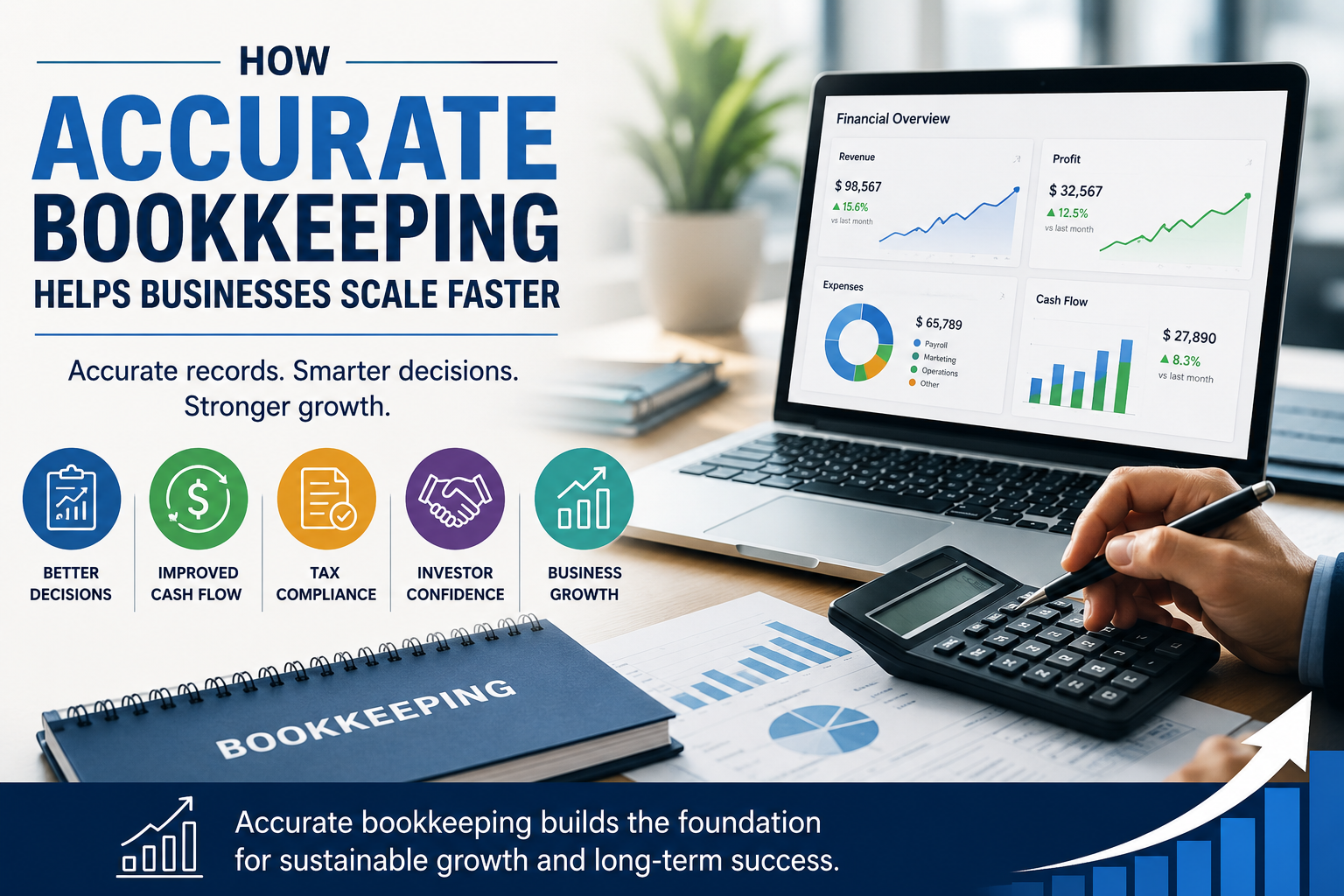

Running a business involves much more than generating sales and managing operations. Behind every successful…

Error: Contact form not found.

The great explorer of the truth, the master-builder of human happiness no one rejects dislikes avoids pleasure itself because it is pleasure but because know who do not those how to pursue pleasures rationally encounter consequences that are extremely painful desires to obtain.

Read More